Fundamentally Valuing MakerDAO

Opinions expressed are solely my own and do not express the views or opinions of my employer.

2024 update: It’s interesting to note that 4 years after this post, Dai has a circulation of about $5B vs the projected $2B. In terms of price, we discounted at a 50% rate which means our expected 2024 price target is $627 * 1.5⁴, or around $3100. It is interesting to note that MKR today is at $2800.

I initially wrote the below in January 2020, with the aim of giving insight into how I thought about Maker DAO and its valuation. I am posting it now, along with observations on what has happened in the one year since.

Stablecoins

Stablecoins are cryptocurrencies whose value is pegged to a target price, like the US dollar. The final goal is for stablecoins to grow into a standalone currency and take significant market share from fiat currencies due to its ability to be used within the defi ecosystem.

Valuation

We can estimate the amount of wealth stored in fiat at about $90 trillion (courtesy of Multicoin Capital).

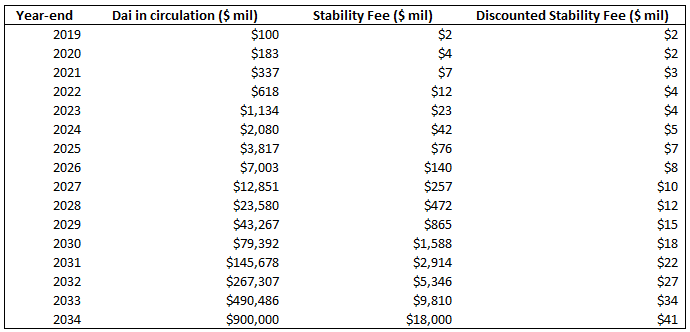

We can make a rough estimate that 1% of this fiat will be taken by the Dai stablecoin in 15 years (a compounded growth rate of 83% from today’s $100 million of Dai in circulation).

A 50% discount rate to account for the investment risk.

There was about $100M of Dai in circulation at the end of 2019.

We can use a discounted cash flow analysis of the fees that accrue to MKR tokens*. Stability fees have ranged from 0.25% to 20%. As of October 2020, Eth-Dai stability fee is 2.0%. We assume 2% stability fee as a long-term average.

*The actual mechanics of MKR value accrual is through token burn, not a dividend

These assumptions would lead to a value of $627 per MKR. Again, this assumes a 50% discount rate to account for the risk involved. Should Maker succeed in grabbing 1% of fiat market share with no major issues along the way (such as massive inflation of MKR tokens due to a black swan event), the ROI at a hypothetical investment price of $627 would be ~287x, as expected of a very successful venture investment. Of course, the end result varies based on the assumptions used.

More here for those who would like to play around with the assumptions: MKR Valuation

Credits to Qiao who posted on Messari using a DCF model to value MKR, which gave me the idea to look at it through this lens. However, I use some different assumptions. I also wanted to point out clearly what “fair value” for a high-risk asset translates to in returns (i.e. $627 is fair value given the extremely high discount rate correlated to risk. If the asset succeeds as projected, the returns will be correspondingly high). For those curious on how the numbers work, the Google Sheets above with cell links and formulas will be helpful.

Looking Back

Today in October 2020, total Dai in circulation is ~$900M — far higher than the projected $180M by 2020 we had at the beginning of the year. It helped that multi-collateral Dai was released, allowing Dai to be generated from more assets like BAT and USDC. This replaced single collateral Dai (now known as Sai) backed solely by Ethereum.

While MKR continues to be volatile and is priced at $545 today, one can expect MKR price to reflect fair value based on fundamentals and Dai’s growing role in crypto. That said, there are many factors affecting MKR including how Ethereum performs, hence investors should expect MKR to be a high-risk investment.

Appendix

Crypto-collateralized

Crypto-collateralized stablecoins maintain its peg by being backed by other cryptoassets. Maker DAO is the most successful case of this.

Maker DAO issues a stablecoin called Dai, pegged to $1 USD. This occurs when one deposits collateral like Ethereum into Maker DAO’s CDP (Collateralized Debt Position) smart contract. At a collateralization ratio of 300%, 100 Dai can be generated from depositing $300 of ETH. The collateral is liquidated when the collateral’s value falls and hits the liquidation ratio of 150%.

CDP creators (those who deposit collateral for Dai) pay an annual stability fee, currently 2% for Ethereum, that goes to holders of the Maker (MKR) token. Think of this as the interest rate for taking a loan by issuing Dai. The stability fee is controlled by a vote of MKR holders, and is critical to maintaining the peg. Simply, if high demand for Dai results in a price greater than $1, the stability fee can be lowered to incentivize more CDPs and increase the supply of Dai, putting downward pressure on the price. When Dai falls below $1, stability fees can be increased to incentivize CDP holders to redeem their collateral and burn their Dai to put upward pressure on the price.

The stability fee is not issued as a cash dividend, but used to burn MKR tokens which serves to increase the valuation of each remaining MKR token, much like a share buyback. In this way, greater adoption of Dai will result in greater value accrual to MKR tokens.

Black Swan Event

If the price of ETH falls rapidly and the CDP becomes undercollateralized, more MKR tokens are created and sold to cover the shortfall. This dilutes the value of MKR. This type of black swan event happened in early 2020.

This is the simple mechanics of how the Maker DAO system works. In practice, it is a very complex system with a network of market participants called keepers that manage the Maker system. Everyday users of Dai do not have to understand this to use the stablecoin — one can just buy Dai stablecoins on an exchange.

Maker DAO Investment and Valuation was originally published in DataDrivenInvestor on Medium.

Before You Go —

To stay updated on new posts like this, follow me on Twitter (@dkSangyoon) and subscribe below!