Observations on Value Fund Managers During Difficult Times

Where some of the greatest learnings can be

I’ve always preferred the concentrated, low-turnover style of investing, sometimes termed value investing, as it allows one to learn a company deeply and invest for the long-term in a handful of businesses. It also aligns with the “Essentialist” way of living, focusing on the few things that truly matter and instead of being busy with a flurry of activities (a reference to the book “Essentialism”). The downside with such an approach can be large drawdowns.

Not much is covered about how the managers think when the funds aren’t performing well, but I think that’s where some of the greatest learnings can be.

Here are some interesting cases I’ve observed on how value fund managers react in a drawdown. I have hyperlinked information on each fund in the titles (underlined).

RV Capital's Letter to Co-Investors for the First Half of 2022

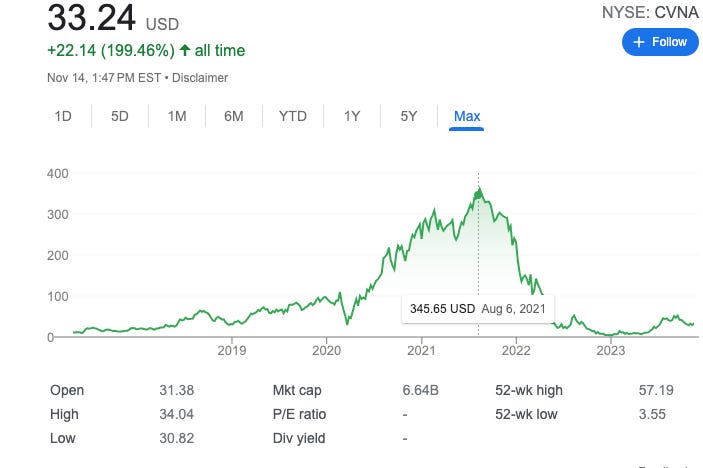

It was interesting to see how this concentrated fund addressed its investors in the middle of a huge drawdown in 2022 (-47% at year end), due to large stakes in companies like Carvana.

First of all, he was very confident in their holdings. To me as an observer, showing that confidence backed by coherent thoughts helps a lot in maintaining my own confidence in the manager. It also helps that the cumulative annualized performance is still good. He was also self-aware, seeing the decline as being caused by both market forces and his own shortcomings.

I find his letter one of the clearest thinkings I’ve encountered, and very relatable. Some parts I liked:

He mentions the Buffett quote about liking falling prices. He says that this presupposes that prices fall in a vacuum, but that is rarely the case. It often occurs due to setbacks at the company, and seeing prices fall before an opinion can be formed on its long-term implications can be stressful. Sharp declines make the bad news feel more plausible too. In the early days, Buffett would buy companies priced below cash balance, or with very clear cash generative abilities, so liking falling prices made sense. There wasn’t much to fear. But when investing in long-duration cash flows like tech stocks, it’s harder to feel confident when prices fall. I found this very grounded, and much more relatable.

He explains that he doesn’t want to overcorrect into cash generative companies now by moving away from tech stocks, and why the latter will recover. 1) Covid led to overspending on infrastructure to meet demand and bloated costs and 2) pull-forward of demand from covid ended. These two factors led to bloated cost and falling growth once covid ended. Even Amazon wasn’t immune to this. However, companies are adaptable - they are cutting costs, and demand pull-forward will work its way through the system, after which these companies will look much stronger.

I also appreciated his point on being unable to predict what will happen to inflation, even if that was important. He cites how he publicly predicted runaway inflation from the immense money printing in 2010, but what ensued was a decade teetering on deflation. This reminded me of Howard Marks’ letters where he almost always states that he does not know what will happen.

The takeaway from this is confidence, self-awareness, and clear thinking in explaining the decline. This goes far in maintaining your LPs’ confidence in you as a manager.

I also found his take on Carvana interesting. He admits it has been a traumatic experience, and admits his big mistake - underestimating financial leverage at the company. Yet, he remained optimistic. He says that the customer experience is better in every way, and other companies will not be able to copy its model. He also liked the CEO, who he saw as a decent person completely dedicated to the company he founded. Ultimately, he is confident that the company will come out cash flow breakeven.

Gotham Capital (Joel Greenblatt)

I enjoyed the Masterclass series on investing, particularly the episode with Joel Greenblatt, who is a renowned special situations investor and taught at the Columbia Business School.

“The more you know about how to value a business, the more you can concentrate your investments in those few things where you feel you have an edge. Most academics who look at portfolio management as a science would say that’s wildly risky.” - Joel Greenblatt

Difficulty 1: After starting Gotham in 1985, he immediately had a huge loss (the big dip in the chart above). He invested in eight merger deals across different industries, which felt diversified, but crumbled all at once when the bond markets turned south and made merger financing difficult.

Lesson: It taught him that if he has a concentrated portfolio, he needs to look hard at what the interconnection of that portfolio could be (in this case them all being merger deals that could be affected by one event).

The next year, he was extra conservative, dodged the crash of 1987, and still made 60%. He could have made 100% or more with more risk, but it taught him that if he could do this well while being very conservative, conservatism should be a core value.

They had a impressive track record being conservative, turning a profit every year until 1997.

Difficulty 2: In 1998, they lost 5% when the market was up 28%. The next year, they were down 5% again when the market was up 21%. They were just doing what they did, but the market disagreed. He says it’s very hard to stay disciplined when this happens, unless you understand in your bones what you are actually trying to do.

While internet stocks boomed, they stuck to their guns. In 2000, the market was down 10%, but they were up 115%.

Lesson: it’s a rough ride, and that’s why not everyone can do it, but you have to be patient and understand what you’re doing.

“I have a firm, Gotham Capital; we have averaged 40% per year for 20 years. $1,000 would now be $836,683.

Gotham Capital stayed small. We returned outside capital, so we could invest in as many situations as possible (not constrained by size). We are very concentrated. We invest in 5 to 8 securities. Know your companies very well. Why that is more safe than diversifying? You pick your spots. So if your holding period is three to five years and you only have 4 to 6 securities, then you only need one or two ideas a year. That is why I have time to teach this class. It is more fun and it works.” - Joel Greenblatt

Arquitos Capital

A small cap hedge fund that I’ve been following for a couple years. They focused on special situation opportunities in small caps, and had great performance for several years. However, a bad activist investment held over years heavily affected its winning streak.

I thought the manager did a good job explaining the situation over the last couple years, with renewed optimism for the coming years.

Some quotes from their latest letter:

“From the launch in April 2012 through the end of 2017, the fund increased its value exponentially, returning 34% annually after fees and expenses. How did we achieve that initial success? Primarily by investing in small companies going through unique circumstances, special situations, and event driven opportunities…

During that time we started building a position in a very small company named Sitestar. The company traded far below its net asset value, which consisted of cash and real estate. The company also had a profitable but mismanaged internet service provider subsidiary. The thinking was that if I could convince the CEO to monetize the company’s real estate and return those proceeds to investors, we would triple our investment. Thus began a hard lesson and the first major investing mistake in the portfolio. Eventually, we would oust the CEO, take over the company, and attempt to turn the company into a publicly traded investment vehicle. We had some early successes. The company made a lucrative seed investment in a third-party fund and helped launch two other private funds in its early days. I also made two major errors, making a large investment in a real estate subsidiary and an investment in a home services venture. Neither of these worked out and I came away with an expensive learning experience that negatively affected our investors financially.

These issues at Sitestar and its subsequent drop in share price led to our first trough in performance for Arquitos after our extraordinary peak. The fund declined three years in a row from 2018-2020…Our ENDI/Sitestar holding also made the portfolio significantly more volatile. However, even if we adjusted for never owning the company [when ENDI did well, it boosted performance, so he is referring to taking that out], we still had years where we were up by 59%, 73%, 52%, 41%, and 34%. Not a bad five years out of 11, and something I believe can happen again.”

Teton Capital Partners, LLC: Free Fallin’

A HBS case study that recounts real estate private equity fund Teton Capital Partners, led by a successful real estate investor who had never lost money on a deal. When the 2008 financial crisis hit, their $2B fund III incurred losses of $1B, with $600M of capital commitments left. It goes through management’s decision to cut management fees to zero for impaired investments, explaining to LPs their mistakes and what they’d do going forward, and a plan to ultimately return 1.0x the fund by deploying the remaining capital profitably.

It mentions the issue of retaining senior management who could leave due to no more carry in the fund, as well as LPs who might rather take a loss and move on, rather than committing the remaining funds.

Ruane, Cunniff & Goldfarb

The only firm that Buffett recommended his investors to after he shut down his partnership in 1969. In the 45-year period from its inception in 1970 to 2015, the Sequoia Fund earned an annualized return of 14.65% versus the S&P 500's annualized return of 10.93%.

Unfortunately, its highly concentrated position in Valeant, which at one point was 30% of the portfolio, marred its performance from 2016 onwards, heavily impairing its reputation and historical annualized performance. That said, its latest 13F shows $6B in positions so it is continuing to play the game and recover from that saga.

SPO Partners

I think it’s important to not only see success and revival cases, but cases in which firms have shut down. That is not to dismiss the spectacular record of these funds, but merely to show the other side.

SPO Partners was a $5B value oriented fund that shut down in 2018. Nonetheless, they have a terrific track record. You can read more about one of the founders, Bill Oberndorf, here. He met Warren Buffett while a student at Stanford’s business school, which inspired him to pursue value investing. He retired earlier in 2012.

Raising Capital at ShawSpring Partners

This is less a case about managing difficult periods in terms of performance, and more about the considerations and challenges in starting a fund.

ShawSpring is a concentrated fund started in 2014 by an alum of Altimeter Capital, that grew rapidly to a peak of $1B AUM (against ~$300M in net LP inflows, meaning most of it were gains in the portfolio). This HBS case study talks about the early days of raising capital.

Things I found interesting:

Through separately managed accounts, he managed several million dollars for high net worth individuals while studying at HBS, that gave him a track record (in addition to his time as a portfolio manager at Altimeter), ultimately dropping out after his first year to start ShawSpring.

A family office provided $10M in start-up capital, with a 3-year lockup, but would receive 20% of all revenue from ShawSpring. It was a revenue share agreement, not equity ownership.

ShawSpring provides twice a year liquidity after an initial 12-month lockup period, to attract LPs who are committed to long-term investing.

Shawspring charged 1.5% annual management fee on AUM, paid quarterly, and 20% incentive fee on returns over 5% annual non-cumulative hard hurdle rate.

Modified high water mark: if fund suffers loss, the incentive fee in future quarters is reduced to 10% until the fund makes back the loss three times over.

I found the last two points interesting because hypothetically, it lets a fund continue to charge fees even while not performing. For example, if the fund went from $100 to $90 one year, then back to $100 the next year, repeatedly, it would continue to make carry while the LPs make nothing. The reduced incentive fee only somewhat mitigates this. I found this interesting. Fortunately, ShawSpring has done well over the last decade.

The case revolves around whether to accept a $40M investment from a university endowment, which could help stabilize ShawSpring during the riskiest early days, and provide revenue to pay its employees and expenses, but came with onerous terms like:

Not pooling capital with other LPs, but through a Separately Managed Account (SMA) where the endowment retained control of the capital and could liquidate at any time. It would also have full transparency in to Shawspring’s trading activities.

SMAs would tax ShawSpring on income-tax rates, rather than long-term capital gains. Endowments are tax-exempt investors so it does not affect them.

Reduced management and incentive fees over an S&P 500 hurdle.

The case mentions ShawSpring recognizing this last point as an aggressive benchmark, but commonly used by endowments investing in ‘long-only’ portfolios. It would also trigger the '“Most Favored Nation” clause of the seed investor, allowing them the same terms. I found this an interesting case study.